Key Resources

Summary Report

Press release

Oil majors worth more adopting 2˚C pathway, independent stress test finds

Read MoreInfographic

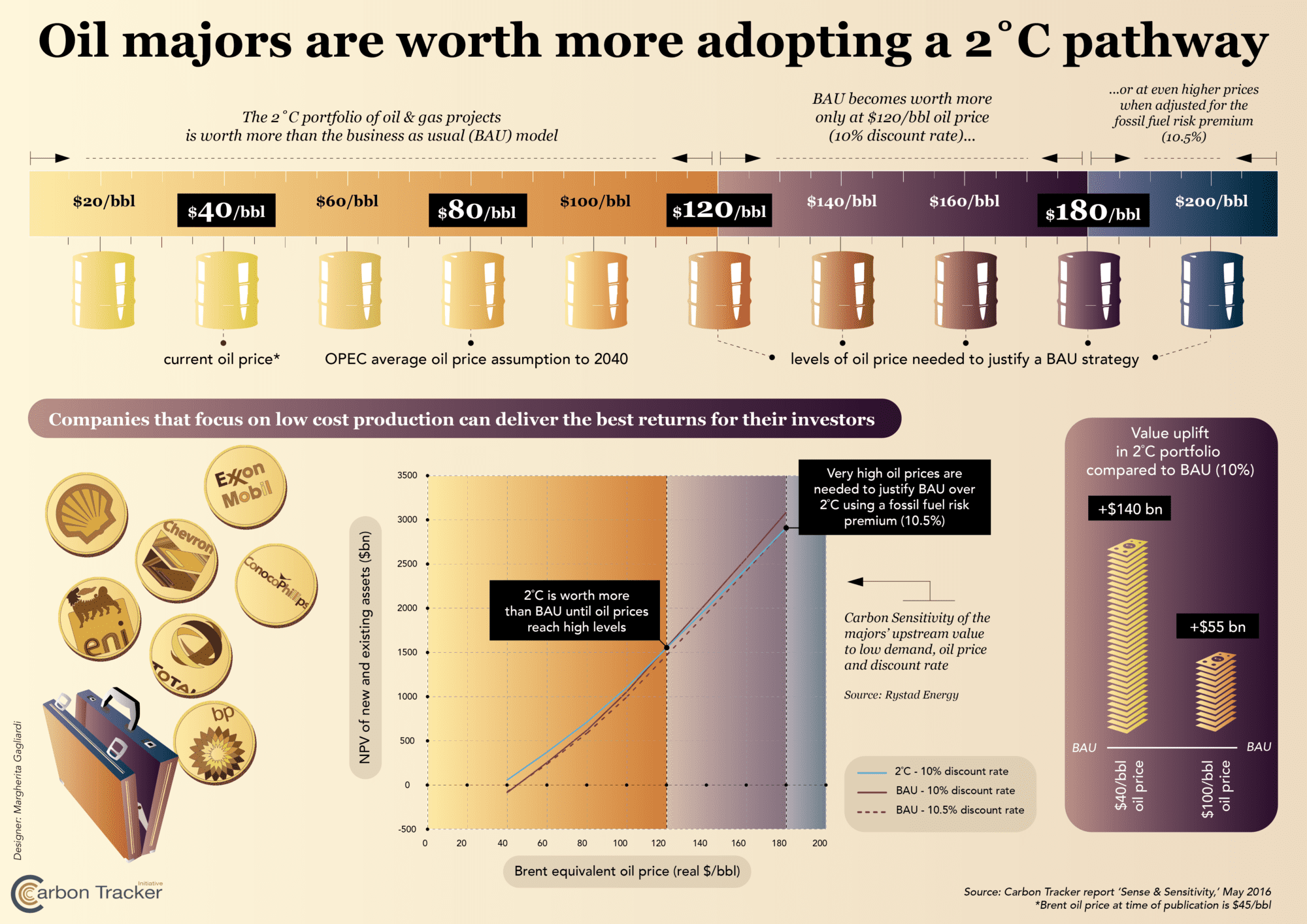

Oil majors are worth more adopting a 2˚C pathway

Download ResourceOil majors could be worth up to $140 billion more by aligning production with climate targets

Key Findings

Carbon sensitivity

Continuing Carbon Tracker’s focus on upstream capex for new oil and gas projects, we have developed a Carbon Sensitivity Analysis. This brings together low carbon demand scenarios with oil price and discount rate sensitivity to understand how reducing exposure to high cost, high carbon projects can optimise value. Given the unpredictability of oil prices, we believe that a sensitivity approach which incorporates a wide range of oil prices (including those that might be thought unlikely at the time) is valuable. This analysis aims to show that it can make financial sense for the oil and gas majors to adopt a strategy of aligning their project portfolios to be consistent with a 2˚C outcome, rather than pursue volume at all costs.

Value creation in a declining demand and production environment

The key comparison is the difference between the net present value (NPV) of a company’s business as usual (BAU) asset portfolio and the low cost subset of that which is consistent with a 2°C warming demand scenario (2D), which implies lower oil production levels for the industry overall. The key question is: “Under which parameters is the NPV of the 2D project portfolio higher than that of the BAU project portfolio?” This has crucial implications for owners who may be surprised at just how much value can be created by oil & gas companies in a carbon-constrained scenario.

2D stress test of new project capex

For the purposes of this exercise, we have examined the portfolios of the oil & gas majors in aggregate, treating them as a single entity. Compared with a BAU portfolio, the oil & gas majors as a group create more shareholder value by managing their future new upstream project developments to be consistent with a 2D demand level at all oil prices up to $120/bbl (in real terms in today’s money, using a 10% discount rate).

Oil price bet

With many commentators now discussing a longer term average oil price of $50-80, far below the levels needed to justify a BAU approach, constraining high cost investment certainly makes sense – as we have seen with the rush to cancel capex on uneconomic developments.

Fossil fuel risk premium

A high cost oil company has a greater risk of failing to pay a dividend or facing bankruptcy. As a result, investors wanting to correctly value low risk companies should use a lower discount rate than they would use for a high cost, high risk investment. Our analysis sets out a method by which a risk-adjusted discount rate or required return can be calculated.

We call this the “fossil fuel risk premium” (FFRP) as it captures the risk associated with a company that invests in high cost projects. When it is applied to the full BAU portfolios of new and existing assets, the analysis suggests that the 2D portfolio outperforms the BAU portfolio at oil prices up to c.$180/bbl as shown in Figure A.

Carbon Sensitivity of NPV of the majors to low demand, oil price and discount rate