Key Resources

Video

The $2 trillion stranded assets danger zone: How fossil fuel firms risk destroying investor returns

Watch VideoPress release

Fossil fuel firms risk wasting $2 trillion on uneconomic projects

Read MoreInfographic

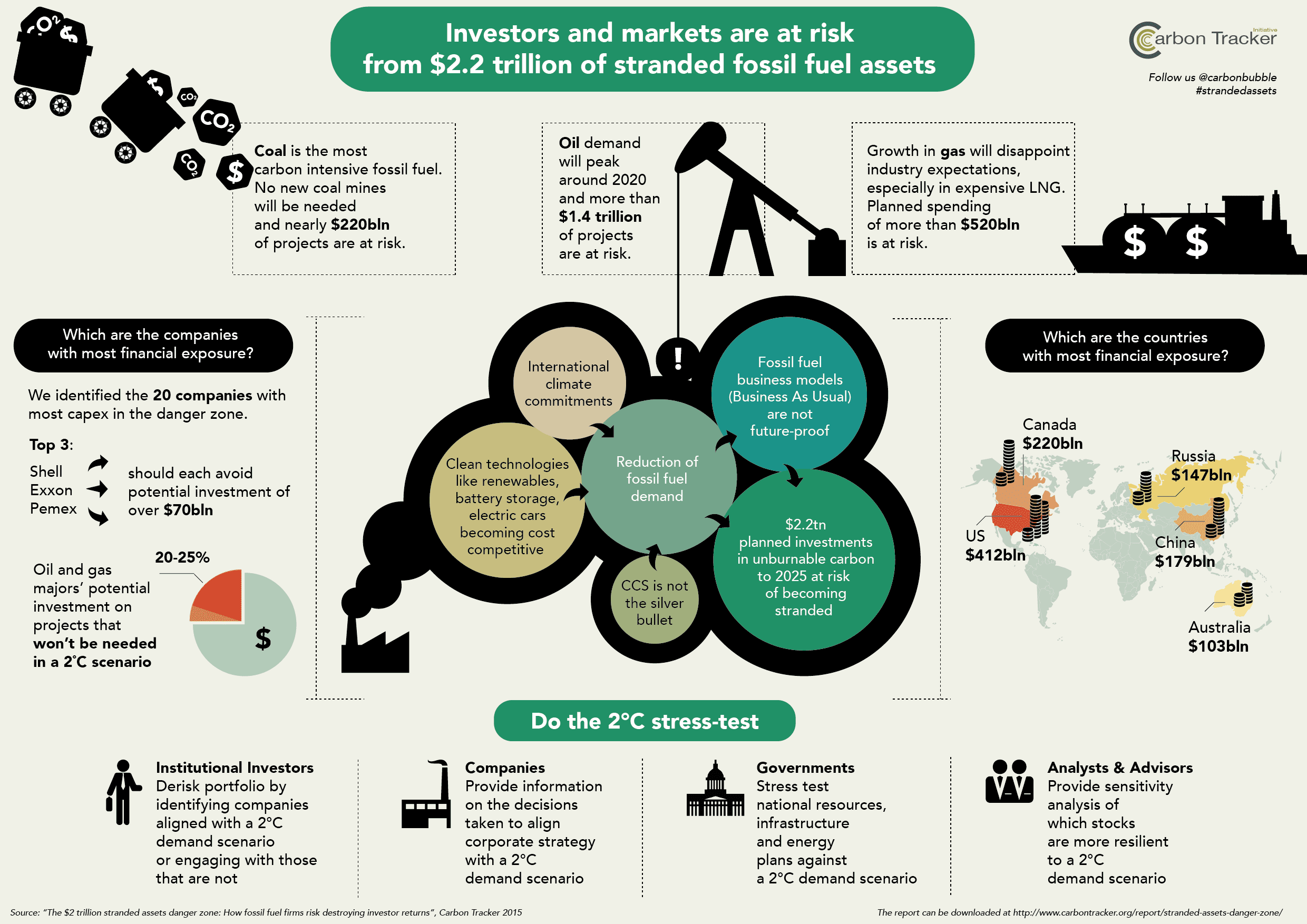

Investors and markets are at risk from $2.2 trillion of stranded fossil fuel assets

Download ResourceMethodology paper

Supporting Paper

Supporting Paper

The data is clear – the energy transition is underway, and the direction of travel is away from fossil fuels. But not everyone will admit that the train has left the station, let alone that it is travelling faster than people expected and may skip some stations along the way.

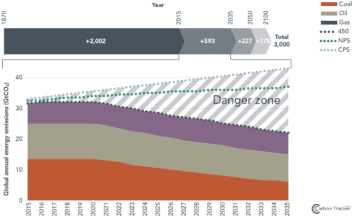

(Nov. 2015) There is a clear danger zone above a 2°C scenario where excess capex and CO2 emissions need to be avoided. All energy players have the chance to navigate around this by staying within the carbon budget. This will give the world an opportunity to reach the ultimate destination – a world that has prevented dangerous levels of climate change. Our analysis here focuses on the marginal production between the IEA 450 Scenario and business as usual for the coal, gas and oil sectors to 2035.

The danger zone above the IEA 450 carbon budget 2015–35

Source: IPCC AR5, IEA WEO 2014, Carbon Tracker

Key Findings

Carbon vs $capex

Greater scrutiny is required for new projects, to take account of 89% of unneeded capex and 67% of avoided CO2. Over $2 trillion of capex needs to not be approved in order to avoid around 156 GtCO2 of emissions – the equivalent of cutting supply and the subsequent emissions by around a quarter in the markets covered in this analysis.

It is clear that oil represents around two-thirds of the financial risk but a fifth of the carbon risk, whilst coal carries around half of the carbon risk, but only a tenth of the financial risk. Gas is low in terms of the carbon risk, but still carries around a quarter of the financial risk.

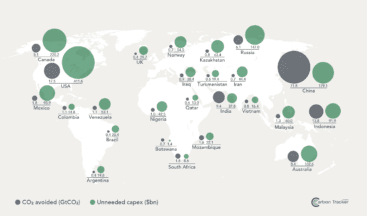

Map of unneeded capex to 2025 and related CO² to 2035 in the danger zone under the 450 scenario (top 25 supply countries)

Source: Carbon Tracker & ETA analysis of Rystad UCube & Wood Mackenzie Ltd GEM

No new coal mines needed

Perhaps the starkest conclusion is that just perpetuating the production from some of the existing coal mines is sufficient to meet the volume of coal required under the 450 scenario. It is the end of the road for expansion of the coal sector.

LNG forming an orderly queue

Gas does not have such a big impact here in terms of determining the climate outcome. Growth is curtailed slightly – especially of capital intensive LNG. This means that the strategies of some companies, especially those operating in the US, Australia, Indonesia, Canada and Malaysia may never come to pass if LNG demand and contracts do not materialise.

Oil facing a culture shock – going ex-growth

The new oil market volatility and uncertainty with OPEC members calling the bluff of the private sector to see who has the marginal production has changed the game. This is seen as an attempt for NOCs to retain market share. This leaves the higher cost US shale oil, Canadian oil sands, Russian conventional oil and Arctic options as traps waiting in the danger zone. It is not Middle East production that is identified in our 2° stress test, as the Gulf States have very little exposure to these types of oil production.

Establishing a benchmark

This analysis established a benchmark of where business as usual sits compared to a 2°C pathway. Going forward: governments need to review energy policies; extractive companies need to review capex plans; and investors need to agree engagement outcomes.