Key Resources

Press Release

US coal crash serves as a warning to investors betting on carbon

Read MoreInfographic

US Coal Crash. Evidence for Structural Change

Download ResourceKey Quotes

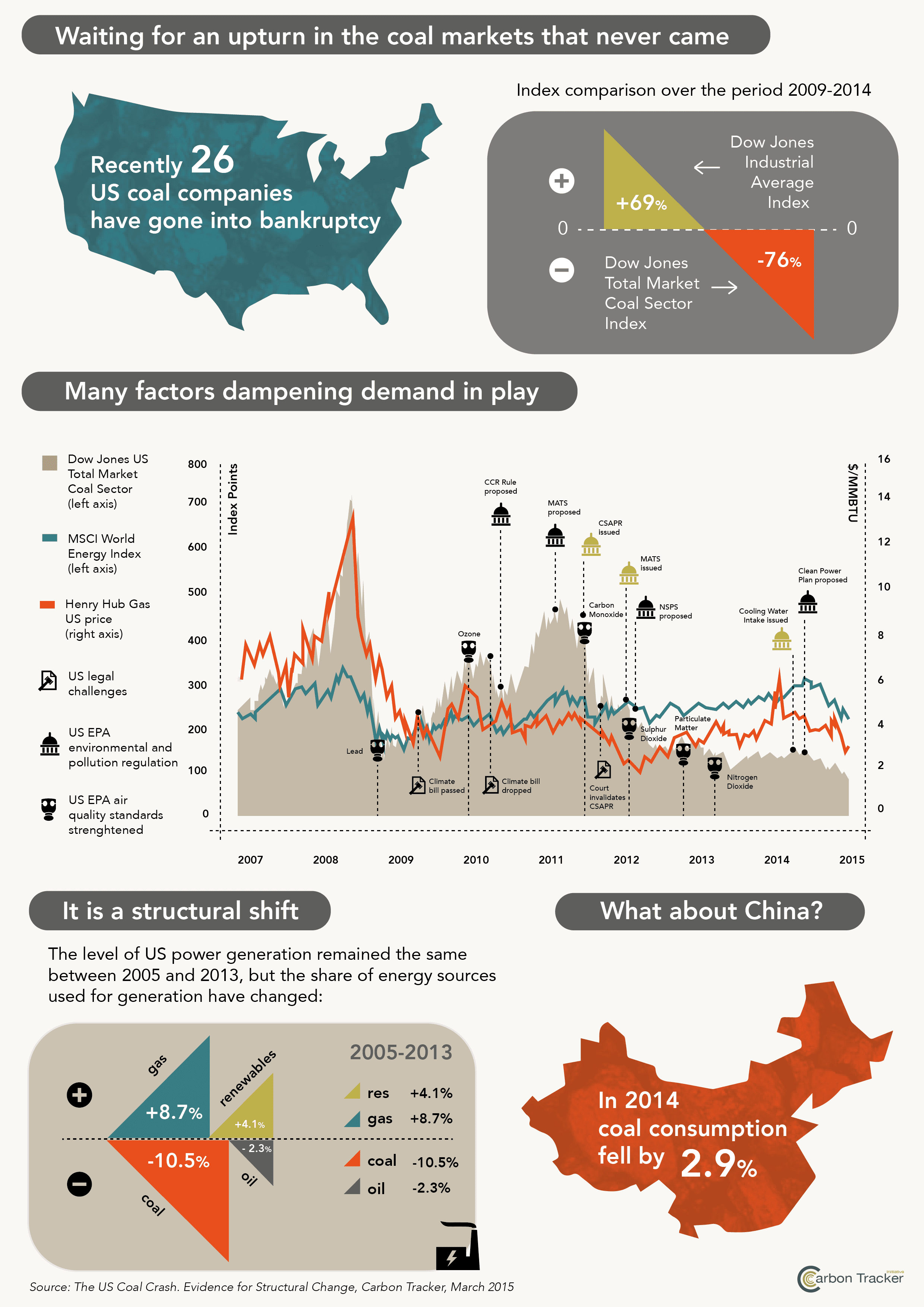

The market for thermal coal is in structural decline in the United States. Squeezed out by an abundance of cheap shale gas and ever tightening pollution laws, it may be a harbinger of things to come for other fossil fuel markets globally.

This report paints a bleak picture and makes grim reading for investors. It finds that in the last few years U.S. coal markets have been pounded by a combination of cheaper renewables, energy efficiency measures, rising construction costs and a rash of legal challenges as well as the shale gas revolution.

Figure: Exploring coal industry index responses to different demand factors (01/01/07 – 20/01/15)

Key Findings

Key takeaways and recommendations

- Whilst historically economic growth in the US has consistently driven increased coal use, there is now clear evidence of a decoupling of the two. In fact, despite GDP continuing to rise, domestic coal use peaked in 2007 and has been on a declining trend since.

- Cheap shale gas has flooded the market in the US, causing the price of natural gas to fall by 80% since 2008 while renewable energy costs have also continued to fall. These two drivers served to reduce coal’s share of electricity supply by approximately 10% over the same period.

- Simultaneously, the US EPA has issued seven environmental, air pollution and climate regulations. These have been significant in continuing to reduce US demand for coal even when the US natural gas price has risen, such as between the start of 2012 and mid-2014.

- These drivers have been the primary reasons behind the stranding of over 14GW of coal-fired power plants between 2010 and 2012 – US thermal coal prices have fallen drastically as a result. The evolution of the US energy sector is far from over, however, as retirements are forecast to rise to 60GW by 2020 and 92GW by 2030, which is equal to 27% of the total US coal generation fleet in 2012.

- This has had a huge impact on the companies engaged in mining it, with over two dozen going bankrupt and many others losing over 80% of their share value over the past three years, including Peabody Energy Corp, the largest producer in the US.

- Albeit localised in this case, this example of a fossil fuel becoming stranded by lower-cost, lower-carbon alternatives and increasing regulations provides an excellent example of how the future may pan out globally and with other fuels as the world moves to a low-carbon economy. Companies and investors by and large underestimated the risks in US coal and did not see the way the wind was blowing until it was too late, and suffered very material losses because of it.

- All of this has occurred without a global climate deal or US federal measures labelled “carbon” or “climate”. Global climate negotiations remain important, of course, and a global deal towards a good climate outcome has never been more desirable, but the changing costs of technologies, and domestic measures on air quality show the building and varied negative pressures on fossil fuel industries.

- Coal’s problems appear to be structural rather than cyclical; accordingly, rather than betting on a cyclical upturn, investors should resist the urge to get back into the US coal sector. We doubt that “business as usual” (as it has previously been understood) will ever return, so investors should seek capital discipline from management and challenge capital expenditure on high-cost projects.

- International investors should also take heed, as the same patterns may play out elsewhere. Timing of fossil fuels being superceded across the various markets will be uncertain, but investors should be cognisant of the dangers and consider their portfolios accordingly – the risk premium of fossil fuel project development has been raised.