Key Resources

This study updates our report 2 Degrees of Separation, and for the first time quantifies risk of overinvestment under a 1.75ᵒC scenario. It was conducted as part of the ET Risk Project funded by the EU Horizon 2020 research and innovation programme.

Oil, gas and thermal coal face varying challenges and degrees of risk in a climate-constrained future. This report looks at each of these fuels in turn with a focus on the upstream end of the value chain, comparing potential supply to a selection of different demand scenarios that result in varying global warming outcomes.

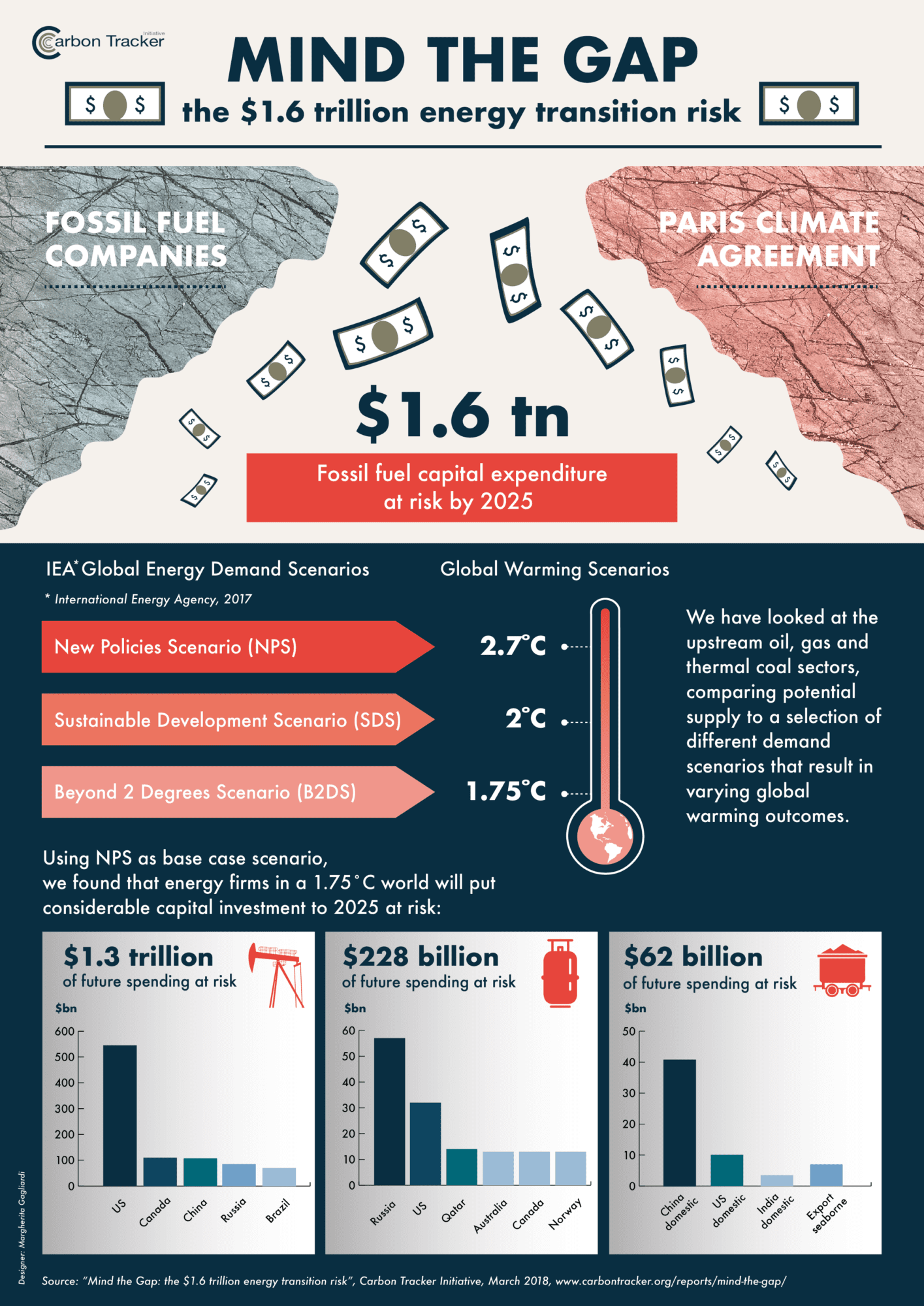

The three scenarios used are drawn from those published annually by the International Energy Agency (IEA). These are the Beyond 2 Degrees Scenario (B2DS, aligned with a 1.75°C global warming outcome); the Sustainable Development Scenario (SDS, aligned with 2°C); and the New Policies Scenario (NPS, aligned with 2.7°C). Each of the scenarios assumes a 50% probability of success in achieving its respective level of warming.

In this report, we have used the NPS level of demand as an upper limit to our potential supply curves. This approach in effect assumes that companies are already aligned with this scenario, and focuses on the “surprise” or “misread” differentials down to the SDS and B2DS demand levels – the capital at risk if companies invest to deliver NPS demand but are caught out by a lower level. We would note that disclosures to date do not suggest that all companies expect long-term demand to be as low as NPS, even if capex levels have been curtailed by prices recently.

Key Findings

- Compared to the SDS, the 1.75°C B2DS demand scenario puts a further $0.7tr capex at risk over the period 2018-2025 for the three fossil fuels (15% of NPS capex). Compared to the NPS, the B2DS requires $1.6tr less capex over the period 2018-2025 (33% of NPS). The SDS requires $0.9tr less (18% of NPS).

- Meeting demand in any of the three scenarios will still require very significant investment. Capital expenditure on existing and new projects in the period 2018-2025 amounts to $3.3tr in the B2DS, $4.0tr in the SDS and $4.8tr in the NPS.

- Coal carries disproportionate danger to the climate, but absolute capex dollars are low compared to oil and gas. Oil and gas account for over 90% of total investment under each scenario, and of the intervals between each scenario.

- New oil and gas projects are needed, but not all of them. Material investment in new oil & gas projects is required even in low demand scenarios – $1.6tr in the B2DS and $2.1tr in the SDS (2018-2025). However, given the multitude of project options available, they also carry the greatest risk. Nearly a quarter of investment dollars in new projects that go ahead in the NPS don’t fit in the SDS, and over 40% of potential capex is surplus to requirements in the B2DS.

- No new thermal coal mines go ahead in the US or China, or to supply the international seaborne export market, in either the SDS or B2DS. This is consistent with prior findings, despite a diminished outlook for potential production.

- No investment in new greenfield oil sands projects is required before 2025 in the B2DS or the SDS

Fossil Fuel Dynamics

Coal has an outsized influence on CO2 emissions, producing around 50% CO2 per unit of energy more than oil and over 60% more than gas.

Accordingly, and due to ease of substitution, in the power sector, thermal coal demand is particularly sensitive to climate outcomes. The B2DS sees 45%

less thermal coal demand globally than the NPS, compared to 14% for gas.

This effect is amplified when looking at new potential projects – no new thermal coal mines at all go ahead in the US, China, or seaborne export market, in either the SDS or B2DS.

However, absolute financial risk is dominated by the oil & gas industry due to its much greater capital intensity – oil & gas accounts for over 90% of the capex in the intervals between the scenarios which are at risk of overinvestment.

![]()

![]()

Who Owns the Risk?

For oil & gas, it is clear that private sector companies and part-listed NOCs have the greatest exposure to the tranches of capex/production lying in the higher risk categories. State-controlled entities that aren’t publicly listed account for just 12% of oil & gas capex in the gap between B2DS and NPS. Oil & gas demand destruction is therefore disproportionately an issue for private investors in capex terms, despite the majority of global reserves being held by national oil companies.

Thermal coal is dominated by state-controlled domestic supply (Chinese and to a lesser degree Indian). However nearly half of the capex of private sector companies falls into the gap between NPS and B2DS demand levels

![]()

![]()

![]()