Key Resources

Press Release

Oil and gas corporates risk future value destruction by rewarding executives for chasing growth

Read MoreReport

Groundhog Pay: How executive incentives trap companies in a loop of fossil growth

Read MoreReport

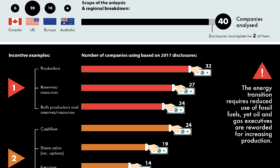

Fanning the Flames: How executives continue to be rewarded to produce more oil and gas at odds with the energy transition

Read MoreInfographic